Domestic Geoarbitrage: The Top 5 cities in the U.S. where $1M feels like $3M. Highlight the undervalued hubs that offer high quality of life with low taxes.

For most Americans, the word “retirement” is synonymous with a massive number (usually a $2 or $3 million portfolio) and a ticking clock that says you can’t stop working until you’re 65. But in the FIRE (Financial Independence, Retire Early) community, we know there’s a massive “cheat code” that can slash years off your working life: Domestic Geoarbitrage.

Geoarbitrage is the simple act of taking a high-cost-of-living (HCOL) income and moving it to a low-cost-of-living (LCOL) area. While many people look to Portugal or Mexico for this, you don’t actually need a passport to make your money go three times further.

If you have $1 million in your 401(k), that money will barely buy a studio in San Francisco or pay the property taxes in New Jersey. But in the right “undervalued” hubs, that same million-dollar portfolio can provide a life of luxury and a safe 4% withdrawal rate that covers everything with room to spare.

Here are the top 5 domestic geoarbitrage hubs where your dollar works as hard as you did to earn it.

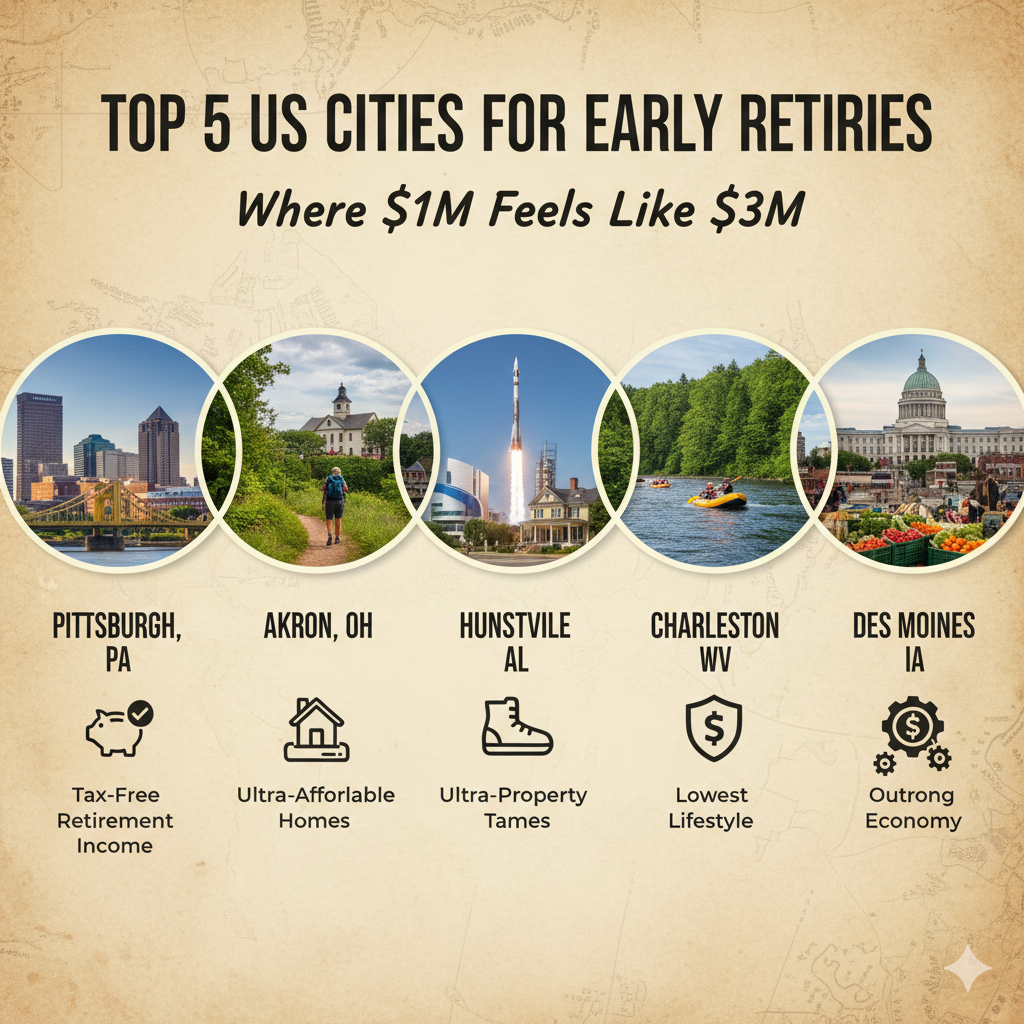

1. Pittsburgh, Pennsylvania: The “steel” city with Gold-Standard value

Pittsburgh has undergone a massive transformation from an industrial center to a tech and healthcare powerhouse. However, unlike Austin or Seattle, its real estate prices haven’t caught up to its quality of life.

- Why it’s a FIRE gem: It is one of the few major U.S. metros where the median home price still hovers around $250,000. Even more critical for early retirees: Pennsylvania does not tax Social Security or most retirement income (like 401(k) and IRA distributions) for residents over 59.5.

- The lifestyle: You get world-class museums, professional sports, and a massive food scene for a fraction of the cost of the East Coast.

- The math: A $1M portfolio at a 4% withdrawal rate ($40,000/year) covers the median annual expenses here with plenty left over for travel.

2. Akron, Ohio: The heart of the “New” Midwest

If you want to maximize your “years of freedom,” Ohio is often the winner. Akron, located just south of Cleveland, consistently ranks as one of the most affordable housing markets in the entire country for 2026.

- Why it’s a FIRE gem: Median home prices in Akron are frequently under $150,000. If you’re coming from Southern California, you could sell a basic 3-bedroom home, buy a mansion in Akron in cash, and still add $500k to your brokerage account.

- The lifestyle: You are minutes away from the Cuyahoga Valley National Park. For early retirees who prioritize hiking, biking, and the outdoors without the “mountain town” price tag, this is a massive win.

- The math: Property taxes are manageable, and the cost of services (contractors, car insurance, groceries) is roughly 20-30% below the national average.

3. Huntsville, Alabama: Low taxes, High IQ

Huntsville is often called “Rocket City” due to its NASA and defense ties. It’s a unique mix of high-earning professionals and incredibly low Southern living costs.

- Why it’s a FIRE gem: Alabama has some of the lowest property taxes in the United States (effective rates around 0.40%). For an early retiree, keeping fixed recurring costs like property tax low is the best way to guard against sequence-of-returns risk.

- The lifestyle: It’s a highly educated city with a booming “Mid-South” culture. You’re also within a day’s drive of the Gulf Coast beaches or the Smoky Mountains.

- The math: $1M in Huntsville doesn’t just feel like $3M; it functions like it because your “tax drag” is virtually non-existent compared to the Northeast or West Coast.

4. Charleston, West Virginia: The Appalachian trail shortcut

Not to be confused with its expensive South Carolina cousin, Charleston, WV, is the ultimate “Deep Value” play. Nestled in the heart of the Appalachian Mountains, it’s perfect for those who want a “mountain retirement” at a 75% discount.

- Why it’s a FIRE Gem: West Virginia has been aggressive in 2026 about attracting remote workers and retirees. The cost of living is nearly 15% below the national average, and housing is so affordable that “Lean FIRE” (retiring on $600k-$800k) is actually realistic here.

- The Lifestyle: This is heaven for outdoor enthusiasts. Whitewater rafting, hiking the Appalachian trail, and rock climbing are your backyard activities.

- The Math: According to recent data, $1 million can last over 18.5 years in West Virginia; nearly double what it would last in Hawaii or California.

5. Des Moines, Iowa: The financial fortress

There’s a reason Des Moines is a hub for the insurance industry; they know how to manage risk and money. For a FIRE practitioner, it’s a city that offers stability and surprising “hipness.”

- Why it’s a FIRE Gem: Des Moines offers a median household income that is high relative to its housing costs. For an early retiree, this means the local economy is robust, but your 401(k) withdrawals go much further at the local grocery store and bistro.

- The Lifestyle: It boasts one of the best-ranked farmers’ markets in the country and a very walkable downtown. It’s clean, safe, and has a “small town feel” with “big city” amenities.

- The Math: Housing costs here are roughly 23% lower than the national average. If you move here from an HCOL area, your “burn rate” drops so significantly that your success probability on a 4% rule jumps toward 100%.

FIRE city comparison: Where your $1M portfolio goes further:

| City | Average Home | Property Tax | Retirement Income Tax | Best “FIRE” Feature |

| Pittsburgh, PA | $255,000 | ~1.5 – 2.0% | Exempt (401k/IRA) | Top-tier healthcare & zero tax on withdrawals. |

| Akron, OH | $155,000 | ~1.4 – 1.6% | Taxable | Lowest barrier to entry for “Lean FIRE.” |

| Huntsville, AL | $310,000 | ~0.40% | Taxable | Rock-bottom recurring carry costs (taxes). |

| Charleston, WV | $165,000 | ~0.60% | Partially Exempt | High “Natural Amenity” value for hikers/bikers. |

| Des Moines, IA | $240,000 | ~1.5 – 1.8% | Exempt (Most Retirement) | Strongest “Recession-Proof” local economy. |

Key takeaways for your 401(k) strategy

- The “Tax trap”: While a city like Akron has incredibly cheap housing, Pennsylvania’s tax exemption on 401(k) and IRA distributions for those over 59.5 can actually save you more money in the long run if you have a massive pre-tax balance.

- The “Carry cost” king: Huntsville wins on property taxes. In high-tax states like New Jersey or Illinois, you might pay $15,000 a year just to “own” your home. In Huntsville, that same home might cost you only $1,500 in taxes, effectively giving you a $13,500 annual raise.

- The “Lifestyle dividend”: Charleston, WV and Akron provide the highest “Lifestyle Dividend”; meaning you get access to National Parks and outdoor recreation that usually costs a premium in states like Colorado or California.

Final thoughts

You don’t need to wait until you have $5 million to retire. By shifting your geography, you can “manufacture” wealth. Moving from a city where a burger costs $22 and a modest home costs $1.2M to a hub like Pittsburgh or Huntsville effectively triples the purchasing power of your 401(k).

Domestic geoarbitrage is about more than just saving money; it’s about buying back your time.

FAQ: Domestic geoarbitrage for FIRE

1. Is property tax the most important factor in choosing a FIRE city? It’s huge, but not the only factor. While Alabama has low property taxes, other states might have higher sales taxes. You need to look at the “Total Tax Burden,” which includes state income tax on your 401(k) withdrawals.

2. Does “cheap” mean “low quality of life”? Not anymore. Many of these “undervalued” hubs have booming tech scenes, craft breweries, and better access to nature than overcrowded coastal cities. The “quality” is often higher because you aren’t spending two hours a day in traffic.

3. What about healthcare for early retirees? This is a valid concern before Medicare kicks in at 65. Cities like Pittsburgh and Des Moines are actually healthcare hubs with world-class hospital systems (like UPMC), ensuring you have great care while you’re “geoadventuring.”

4. How do I test a city before moving? The “Airbnb Test” is the gold standard. Spend a full month in your target city during its “worst” season (e.g., February in Ohio). If you still love the local coffee shops and the vibe when it’s snowing, you’re ready to commit.

5. Will moving to a LCOL area hurt my 401(k) growth? No. Your 401(k) is invested in the market, not your local zip code. In fact, moving to a LCOL area helps your 401(k) because you’ll likely need to withdraw less each year, allowing more of your principal to stay invested and compound over time.

Would you like me to create a comparison table for these cities showing the specific tax rates and median home prices?

The information provided in this article is for informational and educational purposes only and does not constitute financial, legal, or investment advice. While efforts are made to ensure accuracy, Retire ASAP makes no guarantees regarding completeness or applicability to individual circumstances. Readers are encouraged to consult a qualified professional before making any financial decisions.